Multiple panel and CEO-led discussions at the 2025 MedTech conference in San Diego, noted a recent decline in MedTech M&A deals. They also highlighted a decrease in venture financing rounds for MedTech firms and emphasised the growing need for investment in early-stage MedTech companies.

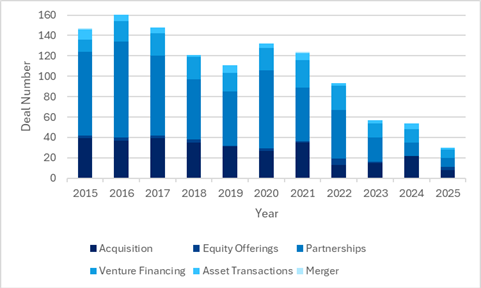

GlobalData analysis supports these conclusions. Figure 1 displays the annual deal count for 15 of the largest MedTech companies starting in 2015. While there is still time for more deals to occur in 2025, there is a notable downward trend in the number of M&A, partnerships, and venture financing deals occurring in recent years.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Although M&A deal volume has decreased, it was noted that the average size of M&A deals in the last few years has risen according to EY’s Pulse of the MedTech Industry Report 2025. This is due to major MedTech companies increasingly favouring acquisitions of more advanced, later-stage companies that possess innovative technologies and align with their broader corporate objectives.

Consistent with the above, GlobalData found that the median M&A deal size for 15 of the top MedTech companies was $895 million in 2021 to 2025, which is over four times higher than the median M&A deal size for the same companies between 2016 and 2020.

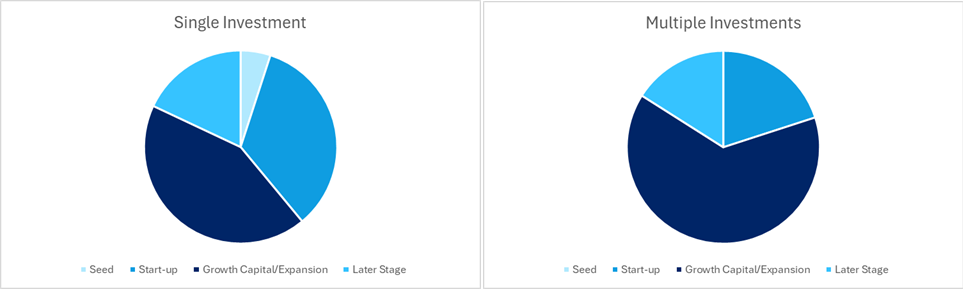

An analysis of GlobalData’s Medical Intelligence Center’s Deals Database reveals that about half of the target companies backed by these MedTech giants have completed multiple successful financing rounds over the past 10 years.

Companies that manage to obtain more than one investment tend to be in growth expansion phases, indicating a robust interest in funding companies expected to scale (Figure 2).

Overall, MedTech companies are strategically concentrating their investments on areas and businesses with strong potential for significant innovation and growth.

Interestingly, to stay aligned with their high-growth strategies, larger MedTech companies are divesting or spinning off divisions that no longer fit their growth objectives.

Over the past 12 months, Medtronic announced plans to spin off its Diabetes business into a standalone company. Similarly, Becton Dickinson & Co revealed it is separating its Biosciences and Diagnostics division, while Johnson & Johnson announced intentions to divest its orthopedic business.

In all three cases, companies cite the same strategic rationale: divesting non-core divisions to streamline their portfolios, allowing each entity to focus on higher‑growth, higher‑margin markets.