In March 2023, a cyclist was disqualified from a road race in Italy after wearing a continuous glucose monitoring (CGM) device. Despite being listed as a banned device in written regulations, it seemed not many knew what the small piece of technology on the cyclist’s arm was doing.

Contrast this to the widespread media coverage surrounding insulin prices, and there seems to be varying attitudes towards diabetes supplies.

Insulin steals limelight

Diabetes imposes a major financial burden on healthcare providers and individuals living with the condition. The NHS in England says it spends around £10bn per year on diabetes – 10% of its entire budget. According to the American Diabetes Association, people with diabetes have medical expenditures nearly two and a half times higher than those who do not have the condition – averaging to nearly $17,000 per person per year.

After much discourse both in public and from within the healthcare sector itself, the Inflation Reduction Act was signed into US law by President Joe Biden in August 2022. It took aim at pharmaceutical manufacturers of insulin – capping the cost of insulin at $35.

Whilst major players such as Eli Lilly, Novo Nordisk and most recently, Sanofi, moved to curb soaring costs and avoid further public backlash, medical devices used by diabetes have not been credited with the same attention.

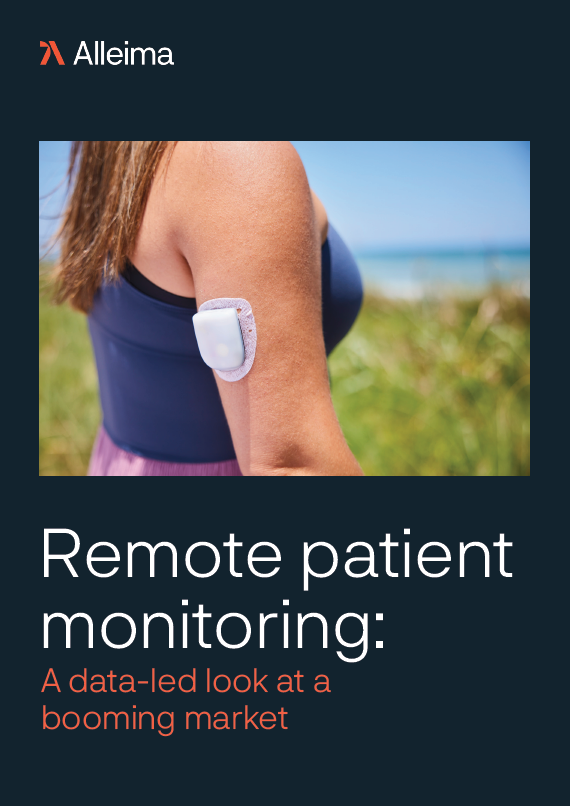

CGM is a category of diabetes medical devices that has seen much technological advancement over the past decade. It is a wearable device that uses a sensor under the skin to measure glucose levels in real-time and then transmits information to a linked handset or mobile phone. It can also be set up with an insulin pump to automatically adjust blood glucose levels.

“A continuous glucose monitor has been very important in my day-to-day life,” says Simon Openshaw, a patient living with Type 1 diabetes (T1D).

“I’ve been using one for five or six years. I can monitor my blood sugar about 15 to 20 times per day and it’s had a significant impact on my short and long-term blood sugar levels. It gives me confidence and helps when out and about cycling or on long walks.”

Patient sentiment towards CGM is overwhelmingly positive – it provides a full and constant analytical picture of glucose levels which can be reviewed, shared, and set up with alarms. But perhaps because they monitor, instead of treating, CGM devices themselves are not permitted equivalent mainstream dialogue.

Whilst their use is recommended, especially for T1D patients, and indeed already widespread, individuals often do not possess complete knowledge of the technology. Diabetes charities like JDRF and Diabetes UK, and social enterprises like DigiBete, are critical in working with the NHS to provide information to people with T1D in a range of settings to build skills, knowledge and confidence around technology choices and access criteria.

An increasing CGM adoption

Whilst CGM devices have roles in both types of diabetes, T1D is the more established application for improving glycaemic control and reducing hypoglycaemia. As technology becomes easier to build and cheaper to deploy, healthcare guidelines have recently facilitated the extensive adoption of CGMs.

In August 2022, NHS England rolled out CGMs to all patients living with T1D. A decade ago, such a widespread scheme would have been unlikely. Technological advancements against a landscape of increasing rates of diabetes diagnoses have steered health institutions to push for CGM allowances.

Medical Device Network spoke to Hilary Nathan, Director of Policy and Communications at JDRF UK, and Lesley Jordan, Technology Access Lead at JDRF UK, a UK diabetes charity.

“90% of people in England and Wales now have access to glucose sensing technologies such as Flash or CGM under the updated 2022 National Institute for Health and Care Excellence (NICE) Guidelines,” says Nathan and Jordan.

“JDRF, along with Diabetes UK and NHS England Diabetes Programme, are scrutinising local commissioning practices to ensure their policies are in line with the 2022 NICE guidance, which states that everyone with T1D in England and Wales should be offered Flash or CGM technology free on the NHS.”

The NHS has placed importance on the deal with Dexcom – the most covered and reimbursed CGM manufacturer in the US – as critical in being able to offer the devices across such a large cohort of people.

“As more and more clinical evidence is collected to show the benefit of CGM use among different populations, indications for use and reimbursement coverage for CGM continues to expand,” Dexcom’s CEO Kevin Sayer tells Medical Device Network.

“Over the past few years, the prevalence of diabetes and prediabetes has been increasing at an alarming rate, with roughly 37.3 million people in the US living with diabetes today. Over the same period, we have also seen a rapid increase in the adoption of CGM with the Dexcom user base growing from 270,000 users at the end of 2017 to 1.7 million users globally at the end of 2022.”

JDRF UK’s Nathan and Jordan explain that advancements in staff training and patient support with technology have helped drive CGM uptake.

“The first factor [driving uptake and adoption] is staff training and their capacity to support people who want to start new technology to learn to use it and feel comfortable with it. The second is providing a range of information, support, peer support so that people can make informed choices,” they say.

Joining the wearable tech wave

It is no surprise that the use, and innovation, of CGMs has gone hand in hand with an increase in popularity of wearable technology. GlobalData predicts the wearable technology sector will be worth $156bn by 2024, with medical wearables being a key driver.

The Covid-19 pandemic shifted patient attitudes toward personal health, with people feeling empowered to manage and monitor health parameters. This sentiment has continued beyond the pandemic and is becoming engrained in health culture today.

A recent proliferation of the mobile health app market is also promoting devices like CGMs – as many of the latest generations can display blood sugar parameters on the user’s phone.

The current technological frontier of blood sugar measuring is attempting to integrate glucose monitoring technology into wearable watches. Apple is reportedly in early developmental stages of adding absorption spectroscopy capabilities to its watches. The K’Watch, developed by PKvitality, uses biosensors through the skin and is currently undergoing clinical trials.

“The launch of the €10 million financed K’Watch has been much anticipated, and the creators will hopefully be launching it at some point within 2023. A CGM watch may disrupt the wearable space due to it not only being of great use to diabetic patients, but it is also a viable means of keeping an eye on your blood sugar for anyone who is health conscious, without having to replace costly CGM devices every few months,” says Shabnam Pervez, analyst at GlobalData, speaking to Medical Device Network.

“Innovations like this are particularly useful for pre-diabetic populations and those who have first-degree relatives with diabetes.”

CGM future potential

A market model by GlobalData illuminates the fruitful future of CGMs, estimating that by 2030, the global CGM market will be worth just over $2bn, up from $600m in 2015.

Companies are continually creating new technologies that are being implemented into monitoring devices. Dexcom, for example, saw its G7 device receive FDA clearance in 2022 and became the first US-cleared device for use by pregnant women with all types of diabetes, including gestational diabetes. The expansion into new markets with new devices, like that of women living with diabetes, is expected to create a more linear application of CGMs.

Innovations in technology will also permit CGMs to confer greater compatibility with automated insulin pumps. The two devices are inherently linked from a therapeutic standpoint, and their markets may drive each other – GlobalData predicts that both the insulin and glucose meter markets combined will be worth $20bn by 2030.

“The future will see a greater range of sensing products and greater interoperability as automated insulin systems are approved by NICE and used by a greater proportion of people with TD1 here in the UK and internationally,” say Nathan and Jordan at JDRF.

The increase in diabetes prevalence is actively driving this market and stronger support from public and private healthcare systems, as well as diabetes charities, are facilitating widespread adoption of diabetes devices and CGM uptake.

“With an increasing proportion of the population developing type 2 diabetes, there will be a proportionate increase in the numbers of people who are insulin dependent, so a greater demand for sensing products. This in turn could help economies of scale and NHS purchasing power,” Nathan and Jordan add.

Ultimately, at a more basic level excluding technological trends, the stability of the diabetes care market relies fundamentally on consistent individual demand.

As Dexcom’s Kevin Sayer explains: “Consumers are increasingly looking for easy-to-use technology that fits seamlessly into their lives and the expectation for medical devices is no different.”