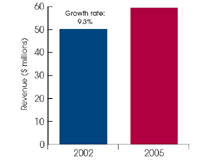

In 2005, the European bone graft market was estimated by Frost &

Sullivan to be worth close to $60m. It is a field that has seen considerable

growth recently. One reason for this is the ageing European population, which

has experienced a rise in age-related musculoskeletal disorders such as

osteoporosis and osteoarthritis.

Another crucial factor contributing to market growth is smoking, which has

an effect on bone density and so influences the occurrence of bone disease.

However, the number of smokers in Europe as a percentage of population has been

decreasing in recent years. As a result, the effects of smoking on the bone

graft market are expected to start diminishing in the future.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

Supplies of allografts from cadavers are limited and cannot always meet

demand, and some other forms of graft, such as hydroxyapatite and demineralised

bone matrix (DBM), are made from allografts. These factors are driving a move

towards bovine bone and synthetic bone grafts.

NEW REGULATIONS FOR BOVINE GRAFTS

In 2004, EU directive 2003/32/EC came into effect, requiring all

manufacturers to undergo additional regulatory assessment procedures before

allowing the introduction of any products using material of animal origin to

the EU market. The new regulations, introduced primarily to minimise the

substantial risk of spreading transmissible spongiform encephalopathies (TSEs),

have been made applicable to all existing and new products.

For bone grafts, the risk of TSE transmission can be minimised by sourcing

tissue from countries free from bovine spongiform encephalopathy (BSE), such as

Australia, New Zealand, Argentina and Brazil. The alternative – putting

tissue through a very harsh process to eliminate disease-carrying prions

– severely affects the mechanical properties of the material and usually

means that it is unsuitable for use as a bone graft.

The enhanced control required by these regulations has had an impact on the

price of bone grafts, as well as their availability. There are now fewer

manufacturers working in this field because of the extra costs of production.

However, bovine bone grafts are still more readily available than allografts

and, with the extra controls, should pose even less risk in terms of

transmitting disease to patients.

PRODUCT DEVELOPMENT AND NEW TRENDS

Manufacturers are increasingly offering new materials and combinations of

existing materials for bone replacement In general, no bone graft substitute is

as good as an autograft. It is only in situations where the patient cannot

undergo an autograft that an alternative is likely to be used. In this case, if

the bone graft is required to provide mechanical strength, bovine bone grafts

are the best option.

Bone grafts made of a combination of bovine collagen and hydroxyapatite

provide mechanical strength and induce new bone growth. If the patient does not

require mechanical support, bioglass offers better results than the more common

hydroxyapatite or DBM.

Since the introduction of bone grafts, surgeons have gradually started using

them instead of the traditional metal plates, pins and screws. However, the

limited clinical application of bone grafts in situations where an allograft

cannot be used has meant that many doctors experienced in using metal implants

do not see the need to learn a new technique for a limited number of

patients.

To change the practice of these surgeons, more positive clinical data

demonstrating the advantages of bone grafts over metal implants are required.

The fact that bone grafts prevent the need for a second surgical site, and do

not require surgery to remove the implant once the bone has healed, has been a

considerable factor in ensuring the widespread uptake of these devices in

recent years.

PROMISING MARKET OUTLOOK

One restraint to further growth of the market is the increasing budgetary

constraint faced by European healthcare providers. Manufactured bone grafts are

more expensive than autografts (which are freely donated by the patient) and

also tend to be more expensive than processed allografts.

However, Frost & Sullivan predicts that the European bone graft market

will continue to grow in the coming years. This is due again to an ageing

population increasing the number of patients requiring manufactured bone

grafts, alongside greater acceptance of these products among clinicians.

While recent regulatory changes have restrained the market, they will ensure

that bone grafts used are safe for the patient. This, in turn, should guarantee

continued confidence in the use of non-human bone grafts.