Medical equipment executives expect to see increased levels of consolidation in their industry in the coming months.

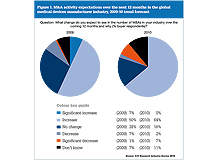

Of respondents to the ICD M&A survey, 64% said there will be either a significant increase or an increase in merger and acquisition (M&A) activity over the next year. Those expecting an increase said ‘attractive valuations / opportunistic takeovers’, ‘growth opportunities’ and ‘survival/increase financial strength’ were the key reasons for the change. As such, cash-rich companies are likely to buy smaller, cash-deficient businesses at a bargain price.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

Opinion among respondents was that a lack of liquidity would result in attractive valuations and more opportunistic takeovers.

Past and present

Executives from medical equipment companies said that, due to the market uncertainty of the past, small companies could find it difficult to sustain the pressures of the credit crunch and might look towards cash-rich companies for survival. This could also lead to attractive valuations/opportunistic takeovers because the smaller companies now have attractive valuations and are available for takeovers.

“In the current climate it is to be expected that small companies will struggle, thus making them more amenable to buy-outs or mergers with larger companies,” said one manufacturer.

In February 2009, Beckman Coulter acquired Tokyo-based Olympus Corporation’s clinical diagnostic testing systems, principally automated chemistry analysers and blood transfusion testing systems. A significant reason for Olympus’s divestiture was anticipated to be swiftly changing dynamics of this segment, which includes intense competition from established and new entrants.

The M&As that took place in 2009 seem to have played a major role in the opinion expressed by survey respondents. During 2009, the consolidations between Abbott Laboratories and Advanced Medical Optics in January, J&J and Mentor Corp, Medtronic and Corevalve in February, Covidien and VNUS Medical Technologies in May, ev3 and Chestnut Medical Technologies in June, Merge Healthcare and Confirms in August, and Corning and Axygen Bioscience in September helped create a positive environment among the medical equipment manufacturing companies.

M&A activity is driven by a powerful surge in demand for more sophisticated medical equipment, led by an ageing population, high patient expectations, more stringent legislation and rising living standards. Investment is focused on key technologies, with changing clinical and surgical practices and also promoting the appeal of consumable products. In the medical devices industry, strategic buyers are interested in growth through innovative technologies and new markets: both might come from a calculated takeover.

According to one North American medical device manufacturer, with the “cyclical trend of industry spawning start-ups, partnerships, acquisitions, attrition and back to start-ups, we’re at the point where numerous start-ups have matured to the point where the successful ones will use acquisitions to continue their growth and the weaker ones will sell out”.

Some companies have strong cash flows whereas others are trying to survive. Hence, this could be the right time for cash-rich companies to acquire at fair prices to achieve strong and profitable growth.

“Small companies with good products will be undervalued and their technology will be desired by big companies to fulfil customer needs rather than to develop in-house,” said one US industry executive.

Purchasing growth

Large companies are trying to grow inorganically through acquisitions as they realise that competition is stiff and they need to reinforce their strength by mergers and acquire other feasible businesses in order to grow faster.

Compared with 2008, the M&A climate for all medical device segments fell in Q2 2009 due to the tight credit and the recessionary economic environment. This was a major reason why none of the survey respondents was expecting a significant increase compared with Q2 2009, where executives had anticipated 7% of significant increase in consolidation.

‘Lack of credit facilities’ and ‘attractive valuation / opportunistic takeovers’ are the two main reasons for increased levels of consolidation in these companies.

Due to unavailability of credit, smaller companies are finding it increasingly difficult to continue with their business operations.

“Because of changes in market dynamics and erosion in bottom-line profits, big companies will be on the lookout for new technologies from start-up companies,” said an Asia Pacific operator. “Small companies would like the support of big companies for their expansion plans, sustain growth and increase market penetration.”

Large cash-rich players could inevitably target struggling smaller companies because those firms, with high-quality equipment, are seeing fewer opportunities, whereas larger companies are seeking their intellectual knowledge.

Supplying the change

Overall, executives from medical equipment supplier companies expect to see increased levels of consolidation with almost half (49%) of respondents predicting an increase in M&A activity over the next 12 months.

An interesting aspect is that the result matches with Q2 2009, where 48% of industry executives had anticipated either a significant increase or an increase in consolidation over the year. Reasons cited are similar to those of the buyers. Attractive valuation / opportunistic takeover was the most important reason for M&A activities, because many good firms are available at a bargain price. ‘Survival / increase financial strength’ and ‘increasing market share’ were other important drivers.

An interesting trend is observed among suppliers where a fifth (20%) of respondents was unsure about the direction in which M&As would move in the industry, despite that only 11% of respondents expected M&As to fall over the next 12 months.

There are few projects undertaken by smaller companies, which could not be completed due to capital constraints, hence large businesses could acquire these at cheaper valuations and complete the stalled projects to attract a wider group of clients. According to one CEO of a supplier operating in Asia Pacific, “larger business houses will buy out smaller ones to reduce completion and increase market share, smaller ones will sell off due to financial pressure and reduced product developments and competition”.

Among those forecasting decreased levels of M&As, respondents felt that in times of recession, a ‘lack of credit availability’ along with ‘market uncertainty’ could be a major factor deterring the companies from acquisitions.

“Smaller companies will need to expand through R&D of innovative products, thus extra capital is needed and M&As provide a faster way to achieve target,” said one CEO.

Overall, despite mixed sentiments, the opinions of industry experts indicate a possible increase in M&A activities over the next year.

Changing horizons

M&As are changing the competitive landscape in the medical devices industry where consolidation of merged organisations is swayed by different influences and stakeholders have many strategic issues to consider. Well-established medical device companies are constantly looking at acquiring comparatively smaller firms in order to support their R&D efforts and to expand their product portfolios.

Shifting disease patterns and an ageing population are great positive drivers for the medical devices market. Growing collaboration among the fields of information technology, medical imaging, pharmaceuticals and medical devices could grow in the future as such synergies have the possibility of producing therapies with unprecedented clinical benefits.