Ophthalmic devices are used to correct vision problems such as myopia, hyperopia, astigmatism, presbyopia, diabetic retinopathy, age-related macular degeneration and cataracts.

Depending on the diagnosis, an ophthalmologist may prescribe drugs or use devices. In the case of devices, the ophthalmologist chooses either surgery (cataract or refractive), devices alone, or a combination of the two. Factors such as patient affordability, the availability of reimbursement, the availability of products, ophthalmologist skill, patient compliance and comfort levels influence the treatment options.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

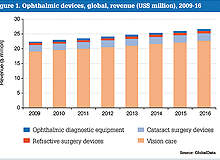

The global market for ophthalmic devices was valued at $23.5 billion in 2009, and is forecast to grow at a compound annual growth rate (CAGR) of 2.5%, reaching $27.9 billion in 2016 (Figures 1 and 2). The market is expected to be driven by a continued increase in the patient population with eye problems, the availability of reimbursement and the direct-to-consumer marketing approach of the ophthalmic device companies.

Opthalmic devices market drivers

A huge proportion of the global population suffers from eye problems and this is expected to drive future demand. About 52% of people have some form of myopia or hyperopia.

In the US, vision impairment and eye disease costs $68 billion a year, before lost productivity, reduced independence, diminished quality of life, increased depression and accelerated mortality are taken into account.

The number of blind or visually impaired Americans aged 40 and older is expected to grow to about 5.5 million in 2020 if proper measures are not taken.

Around 15 million procedures are carried out every year to treat cataracts, the leading cause of blindness worldwide. Some 30 million people suffer age-related macular degeneration, and this number is expected to triple in the next 25 years.

Diabetic retinopathy, meanwhile, causes between 12,000 and 24,000 new cases of blindness each year. This makes diabetes the leading cause of new cases of blindness in adults aged 20-74. The condition is a cause of severe concern in India and China, the two countries with the largest diabetic populations in the world.

Early diagnosis of diabetic retinopathy and timely treatment significantly reduce the risk of vision loss; however, as many as 50% of diabetic patients are not getting their eyes examined or are diagnosed too late for treatment to be effective. About 61 million people are estimated to have glaucoma, and this number is expected to increase to 80 million by 2020.

The fashionable aspect of vision care devices is also leading to high replacement rates, resulting in an increase in market size. Contact lenses are witnessing huge demand as they are, affordable, have a negligible chance of being damaged during a patients’ daily routine and conform to their individual eye shape, with growth driven by newer designs and increased adoption among younger wearers. Coloured contact lenses are among the most popular, and the fact that they can be worn by people with perfect vision is helping to expand the market.

Market restraints

Growth in capital equipment sales, including those for ophthalmic lasers, is limited by low economic growth in developed economies. Tight credit conditions are only worsening the problem by restricting the access to funding for hospitals, clinics and physicians’ offices. Another negative trend is that cash-rich healthcare facilities are delaying their purchases. Reduced expectations on patient volumes, expected healthcare reforms and reimbursement cuts are leading to delays in the purchase of lasers.

Only about 25% of the global population has access to vision correction, stalling market growth. Globally, the current rate of lens adoption is about 25%, whereas 65% of the population actually should be using them. Although accessibility to vision care is very high in developed economies and the urban areas of developing economies, the problem is acute in under-developed economies and the rural areas of developing economies. Low affordability, the slow expansion of healthcare insurance and reduced public and private sector spending is limiting access to vision care in these areas.

The number of patients seeking cataract surgery has increased significantly in Europe over the past two decades. This is resulting in long waiting times, particularly in countries with publicly funded healthcare systems.

In the UK and Canada, patients wait for more than six months for cataract surgery and about ten months for surgery on their second eye. This is limiting market growth despite an increase in the number of patients requiring cataract surgery. The problem is being compounded by a lack of ophthalmologists performing cataract surgery; their numbers have not increased by the same proportion as the number of patients seeking the procedure.

Opthalmic devices: trends and developments

Accommodating intraocular lenses (IOL) provide patients with the ability to focus at multiple distances without glasses or contact lenses. Toric IOLs, which provide the most predictable and stable correction for corneal astigmatism, are the fastest growing premium IOLs, increasing year-on-year as physicians become more comfortable with the technology.

The growth is fuelled by increasing patient demand, especially from those who previously have undergone refractive surgery. Companies are also improving their product offerings in a significant manner, which makes it easy for physicians to implant them. The high affordability of cataract surgery is increasing the number of procedures performed. IOLs can cost as little as $15, and the surgery is considered one of the most cost effective in the developing world. It is also the most requested procedure in the US and Western Europe.

The surgery is particularly popular in economies such as India; of the five million cataract surgeries performed in the country each year, four million involved IOL implantation. Affordability and availability have set India on the path to becoming the largest consumer of IOLs in the world.

Micro-incision cataract surgery, which allows surgeons to implant an IOL through an incision of just 1.8mm, has been greatly enabled by the advent of new phacoemulsification platforms and foldable IOLs. The overall number of micro-incision cataract surgeries performed each year is increasing, in part due its advantages, which include no surgery-induced astigmatisms, immediate visual recovery, less trauma, low risk of endothelial cell loss and rapid wound healing.

Femtosecond lasers have also become a versatile tool for reshaping the cornea. These lasers, previously used as alternatives to microkeratomes for making Laser-Assisted In Situ Keratomileusis flaps, can now cut oval flaps, vary the shape of side cuts, perform cuts for keratoplasty procedures and create intrastromal refractive changes. Femtosecond lasers are gaining greater traction as they surpass microkeratomes in safety and usefulness.

Optical coherence tomography (OCT) is being increasingly adopted, specifically for spectral domain high resolution. OCT works by measuring the echoed time delays of a reflected light beam. A cross-sectional image is generated when the beam is scanned. The higher imaging speed of OCT allows for higher pixel densities and better image quality, with a consequent improvement in diagnosis.

The technology affords a better understanding of the pathogenesis of retinal disease, and enables sensitive diagnosis. It also allows health professionals to monitor disease progression and response to therapy.

One of the key developments in the spectacle lens market has been in materials, particularly plastics. The availability of a wide range of refractive indices has coincided with the fashion trend for smaller spectacle frames, which have made the requirement for higher refractive index materials less daunting. The increase in the popularity of plastic lenses is related to their inherently superior strength in comparison to glass.

Direct-to-consumer approach pays off

The majority of the leading companies in the ophthalmic devices market are engaged in direct-to-consumer (DTC) advertising through television, the internet, magazine coupons and consumer sweepstakes.

The impact of DTC advertising in the contact lens market segment is such that patients often go to their doctor with a coupon for a free trial of a particular contact lens, thereby questioning and limiting the doctor’s choice of prescription lenses.

A good example of how DTC advertising can influence patient preferences concerns the toric lens. Because of poor vision from uncorrected astigmatisms, many patients either avoided or stopped wearing soft contact lenses in the past.

Advances in technology for toric lenses, advertised to consumers directly, are making wearing contact lenses more appealing.

The internet is quickly becoming one of the preferred mediums for DTC advertising. About 80% of all internet users search for health information on the internet, and this is expected to change the way consumers seek health information.

Ophthalmic devices market composition

Essilor was the leader of the global ophthalmic devices market in 2009, with a 17% market share (Figure 3). They were followed by Johnson & Johnson Vision Care (10%), Hoya Corporation (7%), Bausch & Lomb (7%), CIBA Vision (7%), Carl Zeiss (6%) and Alcon (5%).

The ophthalmic devices market is characterised by presence of both local and multinational companies. Local companies, with their competitive pricing and low manufacturing costs, are providing fierce competition for the leading firms.

Essilor International, Johnson & Johnson Vision Care and CIBA Vision Corporation are concentrating their product portfolio in the vision care segment, which accounts for 71% of the overall ophthalmic devices market. These are also the companies that customers associate most with spectacle and contact lenses. Essilor has undertaken about 45 acquisitions in the past four years to strengthen its portfolio in this segment.

Alcon is one of the leaders in the cataract surgery devices and refractive surgery devices categories, and is concentrating more on new product development and organic growth. Carl Zeiss and Bausch & Lomb are exploring organic and inorganic growth opportunities for expanding their product offerings.