The orthopedics market covers a wide range of medical devices, from bone cement and surgical power tools to joint replacement implants and prosthetic limbs, all of which aim to provide patients with increased mobility. Driven largely by the aging population and patients’ desire to maintain an active lifestyle, the global orthopedics market was valued at $52.7B in 2017. GlobalData expects this market will grow to $66.3B in 2023 at a steady Compound Annual Growth Rate (CAGR) of 3.9%.

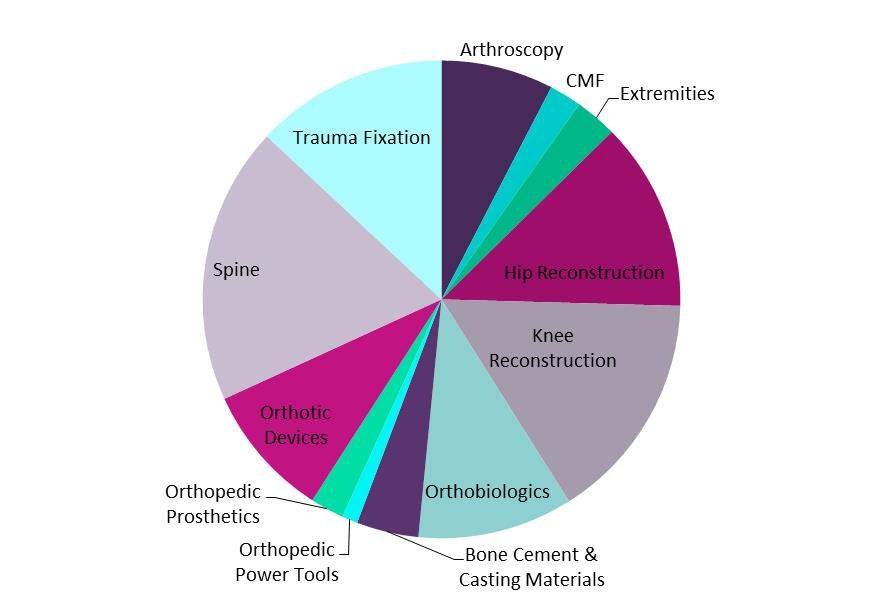

The largest market segments in 2017 were spine devices, hip and knee reconstruction implants, and trauma fixation. These markets are mature and established, with growth largely driven by the aging global population and subsequent increasing prevalence of diseases that primarily affect the elderly, including osteoarthritis and osteoporosis. However, the market segment expected to undergo the fastest growth is extremity implants, which is anticipated to grow at a CAGR of 6.2% through the forecast period. This segment covers reconstructive implants for the small joints—ankle, digits, elbow, shoulder, and wrist—and is building on the established success of hip and knee implants. High growth is this area is powered by the increasing awareness of patients and physicians alike of small joint implant options, and technological innovations contributing to more advanced implant designs. The forecast market for extremity implants will be propelled by shoulder and ankle replacement, which are projected to grow at CAGRs of 6.5% and 6.3%, respectively.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The merger and acquisition (M&A) scene in the orthopedics space was relatively calm in 2017. A number of small company and product line acquisitions, many in the spine market, took place in lieu of the large, transformative actions made in recent years. The most notable move was Centinel Spine’s acquisition of DePuy’s Prodisc platform, which includes cervical and lumbar disc replacement systems. Artificial disc replacement is a growing trend worldwide, and Centinel Spine’s plans to expand the number of devices approved in the US market will position the company well for international growth, as GlobalData anticipates the global artificial disc replacement market will grow at a speedy CAGR of 15.1% through 2023.

Moving into 2018, there are several areas to watch that GlobalData anticipates will affect the orthopedics markets. Patient specific implants are expected to drive growth in the hip and knee markets, as is patient specific instrumentation (PSI), a tool developed to improve accuracy in total knee arthroplasty procedures by customizing the surgical cutting blocks to the patient’s anatomy. Similarly in the vein of personalized healthcare, 3D printing in a variety of orthopedic markets, including spinal interbodies, cranimaxillofacial implants, and prosthetic devices, will advance physicians’ ability to provide customized solutions to patients.

Minimally invasive and robotic surgical systems are a growing trend in orthopedic surgeries, and major orthopedic players, including Medtronic, Stryker, Smith & Nephew, and DePuy, are taking steps to ensure they remain competitive with their Mazor X, Mako, NAVIO, and PUREVUE systems, respectively. Lastly, a shift in the US towards value-based healthcare, including Medicare’s Comprehensive Care for Joint Replacement (CJR) model, will continue to impact both orthopedic manufacturers and physicians, as will the move towards outpatient procedures in ambulatory surgical centers (ASCs).